Financing Programs

Working Capital vs. Equipment Financing for Switchgear Buyers

A bank line of credit and an equipment loan both move money. They are not the same tool, and using the wrong one costs you. Drawing your working capital line to buy $400k of switchgear ties up credit you need for payroll, materials procurement, and subcontractor payments, leaving you exposed the next time a job starts three weeks before the first invoice clears. Equipment financing was designed for exactly this purchase, and it leaves the bank line intact for what the bank line is for.

This page is for contractors, industrials, and facility operators who are weighing whether to use an existing credit facility or set up dedicated equipment financing for a medium-voltage switchgear, unit substation, or motor control center purchase.

What Each Tool Is Built For

Working capital lines of credit are revolving facilities designed for short-duration, variable draws. You draw to cover a materials purchase or a payroll cycle, you pay it back when receipts come in. The facility revolves. Rates are typically variable and tied to prime or SOFR. They are efficient for payables management and are terrible for large, long-duration purchases.

Equipment loans and leases are term facilities designed for a specific asset. Fixed payment, fixed term, matched to the useful life of the gear. The equipment secures the loan, which is why equipment financing rates are frequently better than unsecured working capital rates even for the same borrower. The collateral changes the risk calculus.

The practical consequence: equipment financing tends to be cheaper money for the purpose of buying equipment, and it preserves the credit facility you need for day-to-day operations.

When To Use Equipment Financing (Not The Line)

Use dedicated equipment financing when:

- The purchase exceeds 20 to 25 percent of your available line. Drawing that much of a revolving facility for a single long-lived asset crowds out the operational flexibility the line is supposed to provide.

- The equipment will be in service for three or more years. Long service life assets belong in term financing, not revolving credit.

- You want to match the cost of the asset to the revenue it generates over time. A fixed monthly payment on a 60-month term aligns the cost of the gear with the project revenue it supports.

- You are buying gear for an industrial installation that will be productive for decades. Buying it on the line of credit and paying it off over 12 months front-loads all the cost before the asset has earned its keep.

Consider working capital (or some combination) when:

- The purchase is genuinely short-term and will be paid off in under 12 months from project revenue.

- You are buying gear for a specific contract that has a short duration and a quick payoff schedule baked in.

Rate And Cost Comparison

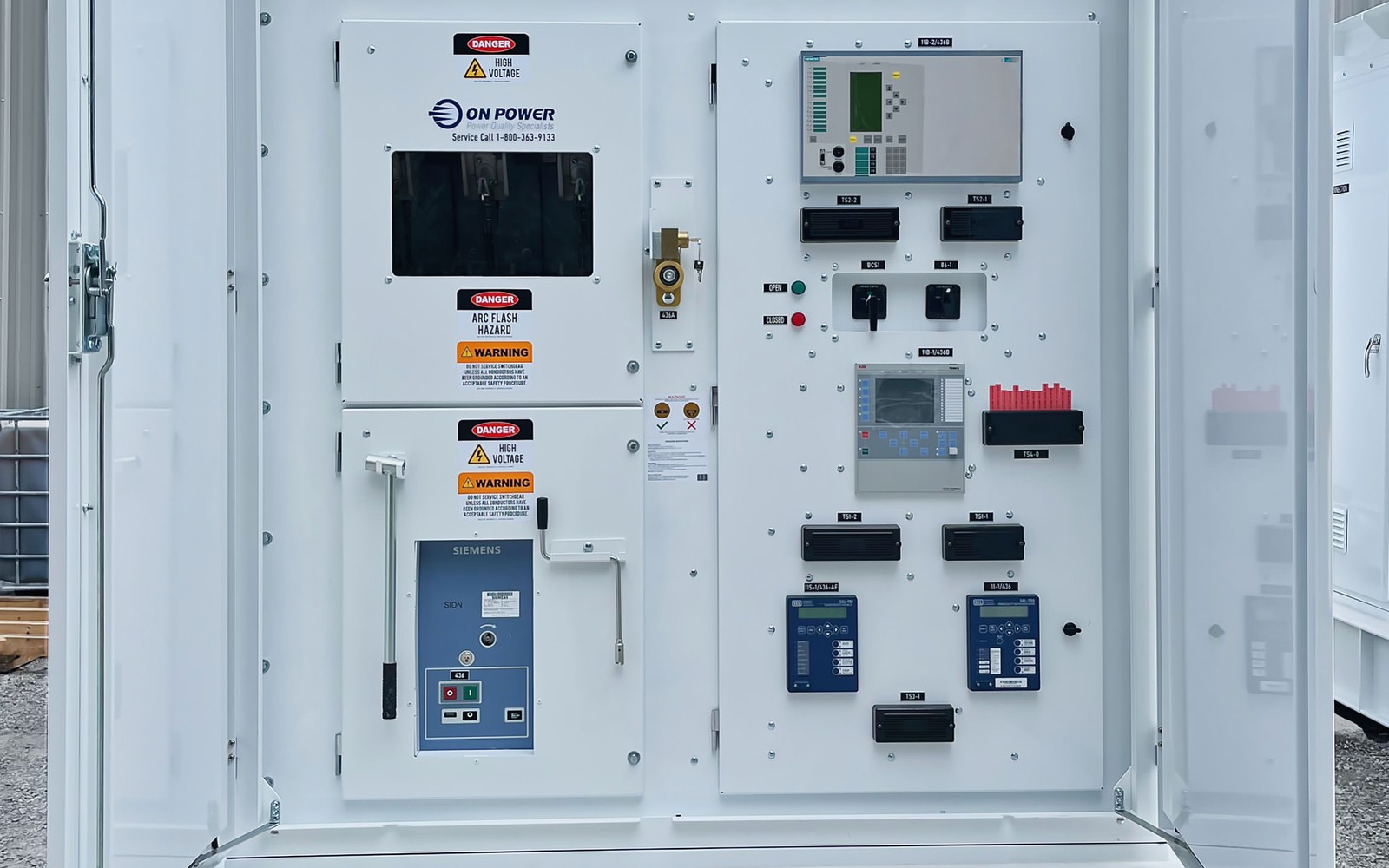

Equipment loans are secured by the asset itself. Unsecured working capital lines are not. Secured financing commands lower rates because the lender can recover the collateral if needed. For a well-maintained asset like a arc-resistant switchgear lineup from Eaton or a ABB substation assembly, lenders are confident in collateral value and price accordingly.

Variable rate working capital lines also carry interest rate risk. A purchase made at 8 percent on the line can become a 10 or 11 percent cost if rates move before you pay it off. Fixed-rate equipment financing locks you in regardless of what rates do after closing. For a $300k purchase, that certainty has real value over a 48 or 60-month payback period.

One nuance: origination fees on equipment loans add to the effective cost. Working capital lines typically have lower closing costs. Factor both into the total cost of funds comparison, not just the stated rate.

Using Both Tools Together

Many well-run contractors use both at the same time for different purposes. Equipment financing covers the gear. The bank line covers float. This is not financial complexity for its own sake. It is the right tool for each job.

For a project-driven business, a contractor might use progress and deposit financing to fund gear procurement deposits, hold the bank line for subcontractor payments and materials, and close out the equipment loan when the project wraps. Each tool plays its role. None of them crowd out the others.

If you serve data centers or renewable energy developers, your projects often have defined timelines and milestone-based billing. Equipment financing matched to that timeline keeps the financial structure clean and predictable throughout the project cycle.

Price This Switchgear Financing Package

Send the quote, seller, lead time, deposit requirement, project location, and the electrical package scope. We will review the structure around the purchase schedule.

Review Switchgear TermsCommon Questions on Working Capital vs. Equipment Financing for Switchgear Buyers

Straight answers before you send the equipment file.

My bank says I can use my line of credit for equipment. Why would I not?

Convenience is the main argument for using the line. The counterarguments are rate risk on variable lines, credit facility capacity erosion for a long-lived asset, and the fact that equipment financing rates are often competitive with secured line rates. Run the comparison before deciding.

Can I pay off an equipment loan early if I want to?

Most equipment loans allow early payoff, sometimes with a prepayment fee in the first 12 to 24 months. Check the specific loan agreement before assuming you can pay it off for free. Some lenders charge a yield maintenance fee that can be meaningful.

Does using equipment financing instead of the bank line improve my borrowing capacity?

It keeps the bank line available for its intended purpose, which means you are not forced to reduce operations or delay other purchases because one asset exhausted your revolving facility. In that sense, yes, it preserves effective capacity.

What if I need both working capital and new equipment at the same time?

The two can be addressed simultaneously. Equipment financing for the gear, and if you need additional working capital, a separate short-term line or merchant-advance-type product for cash flow. We focus on the equipment side and can refer you to working capital sources if needed.

Is there a minimum project size where equipment financing starts to make sense over the line?

There is no hard floor, but transactions under $50k often make more sense on a credit card or short-term line because the fixed costs of setting up an equipment loan are proportionally high. Our minimum is $50k, and the cost-benefit of a dedicated loan gets stronger as the purchase size grows.

Review The Working Capital vs. Equipment Financing for Switchgear Buyers Package

Send the equipment quote, seller, lead time, deposit schedule, and project location. The finance desk will review the package against the actual procurement calendar.