Financing Programs

Bonus Depreciation Financing for Switchgear

Bonus depreciation lets you front-load the tax deduction on qualifying equipment into year one, rather than spreading it across a 5 or 7-year MACRS schedule. Combined with financing, the result is an immediate large deduction and a spread-out payment, which is a materially better outcome than either paying cash (no spread) or not taking the deduction (no tax benefit). For buyers of switchgear and electrical infrastructure, the numbers involved make bonus depreciation worth understanding before you close.

This page covers how bonus depreciation applies to financed medium-voltage switchgear, motor control centers, unit substations, and related power distribution assets, and how to structure the financing to take full advantage of the deduction.

Bonus Depreciation On Financed Equipment

Bonus depreciation (technically the Special Depreciation Allowance under IRC Section 168(k)) allows a specified percentage of an asset's cost to be deducted in the first year the asset is placed in service. That percentage has changed several times through tax legislation and has been subject to phase-down schedules since 2023. Confirm the current percentage with your CPA because it is not fixed.

What does not change: the deduction applies to financed equipment the same as paid-in-full equipment. You do not need to own the asset free and clear to take bonus depreciation. You need to own it, meaning a loan works and an operating lease does not. A dollar buyout lease may qualify because it transfers effective ownership.

The practical structure for a switchgear buyer:

- Finance the gear with a 60-month equipment loan.

- Gear is placed in service in the current tax year.

- CPA takes the applicable bonus depreciation percentage as a deduction in year one.

- Remaining basis, if any, goes on the standard MACRS schedule.

- You pay off the loan over years one through five.

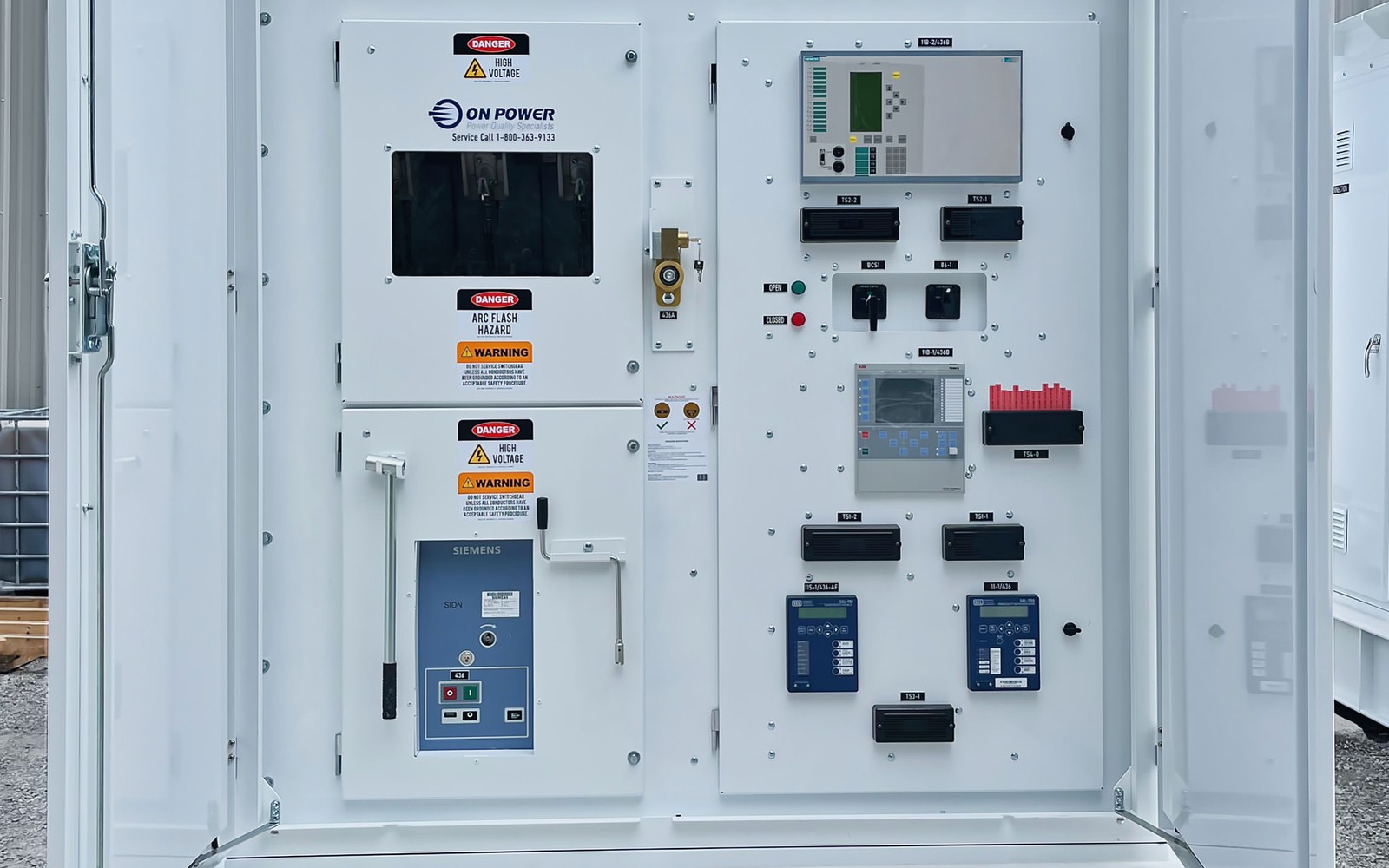

What Electrical Gear Qualifies For Bonus Depreciation

Most power distribution equipment placed in service as tangible personal property in a business qualifies. The equipment must have a MACRS recovery period of 20 years or less, which covers essentially all switchgear and electrical distribution assets:

- Low-voltage switchgear and arc-resistant switchgear

- Automatic transfer switches and paralleling switchgear

- Dry-type transformers and variable frequency drives

- UPS systems and power conditioning assemblies

Used equipment qualifies for bonus depreciation under current law if it is new to the taxpayer and meets the other criteria. This differs from the historical treatment under prior law, which restricted bonus depreciation to new equipment only. Confirm current law treatment with your CPA.

Real property components, meaning anything that qualifies as a structural improvement rather than personal property, does not qualify. A pad-mounted switchgear building might have components that straddle this line. The equipment inside qualifies. The permanent concrete pad and foundation may not.

Combining Bonus Depreciation And Section 179

Bonus depreciation and Section 179 can be used on the same transaction in combination, though the order of application matters and the interaction has specific rules. Generally, Section 179 is applied first (up to the annual limit and the taxable income cap), and bonus depreciation covers any remaining basis above the Section 179 ceiling or in excess of the income cap.

One advantage of bonus depreciation over Section 179: bonus depreciation can create or increase a net operating loss, which can then be carried back or forward. Section 179 cannot create a loss. For a business with a substantial equipment purchase in a strong revenue year, layering both tools under CPA guidance can maximize the year-one tax benefit.

Timing And The Phase-Down

Bonus depreciation has been subject to a phase-down schedule. The percentage was 100 percent for equipment placed in service through 2022, then began stepping down. The specific rate for the current year matters to the math. Buyers who are evaluating a large switchgear or substation purchase and want to use bonus depreciation should confirm both the current percentage and whether legislative changes are anticipated before they close.

The timing of energization matters. Placed-in-service for electrical gear generally means the system is installed, commissioned, and ready for its intended use. For gear from manufacturers like Siemens, Powell, or Caterpillar with multi-month lead times, start the conversation with both your equipment vendor and your CPA well before the fiscal year-end to confirm that delivery and commissioning can happen within the target tax year.

Price This Switchgear Financing Package

Send the quote, seller, lead time, deposit requirement, project location, and the electrical package scope. We will review the structure around the purchase schedule.

Review Switchgear TermsCommon Questions on Bonus Depreciation Financing for Switchgear

Straight answers before you send the equipment file.

Does bonus depreciation apply to equipment I lease, or only equipment I own?

Bonus depreciation applies to owned equipment. True operating leases do not transfer ownership, so they are not eligible. Dollar buyout leases, which are economically similar to loans, may qualify. Your CPA determines whether a specific lease structure meets the ownership test.

We are buying $1.2 million of switchgear. Does the bonus depreciation apply to the full amount?

It applies to the full placed-in-service basis, assuming the current-year bonus depreciation percentage and the qualifying property requirements are both met. There is no per-asset cap on bonus depreciation, unlike Section 179 which has an annual ceiling.

What if our fiscal year ends in June, not December?

The placed-in-service date corresponds to your tax year, not the calendar year. Equipment placed in service in your fiscal year ending June 30 takes the deduction on the return for that fiscal year. Confirm the exact interaction with your CPA because the bonus depreciation phase-down percentages are tied to calendar years in some cases.

Can bonus depreciation create a tax loss that carries to a future year?

Yes, under current law. A net operating loss from bonus depreciation can be carried forward indefinitely, though the carryforward rules have specific limits under current tax law. Section 179 by contrast cannot create a loss. Bonus depreciation is the tool for a purchase that exceeds current-year taxable income.

My lender wants a personal guarantee. Does that affect the ownership question for bonus depreciation?

No. A personal guarantee on an equipment loan is a credit requirement, not an ownership issue. The borrowing entity (your business) owns the asset. The personal guarantee is separate from the tax treatment of the asset's depreciation.

Review The Bonus Depreciation Financing for Switchgear Package

Send the equipment quote, seller, lead time, deposit schedule, and project location. The finance desk will review the package against the actual procurement calendar.