Financing Programs

Cash-Out Refinancing for Switchgear

Switchgear appreciates against its original loan balance as payments reduce principal. If the equipment has been in service for a few years and holds solid market value, a cash-out refinance replaces the existing loan with a new, larger one. The old balance gets paid off. The difference lands in your account. You keep the gear and keep operating.

This structure works best when the equipment appraised value is meaningfully higher than the remaining loan balance. The gap between those two numbers is your equity, and a cash-out refi converts some of that equity to cash without a sale. We work this structure on medium-voltage switchgear, low-voltage switchgear, pad-mounted transformers, and complete substation assemblies.

The practical appeal is direct: you get working capital without taking on unsecured debt at higher rates, without selling the equipment, and without disrupting the operation that depends on the gear staying in place. For companies in between billing milestones or trying to fund a new project while existing equipment is earning, cash-out refinancing is a mechanism that banks rarely offer on equipment and that most business owners do not know exists until they ask.

Mechanics Of A Cash-Out Refi On Electrical Gear

The transaction works like this: a lender appraises the gear, advances a new loan against that value (typically 75 to 85 percent of appraised value), uses the proceeds to pay off the existing lender, and wires the balance to you at closing. Your new payment reflects the higher principal and the new term.

Example: You have switchgear that originally financed at $300,000. Current payoff is $90,000. An appraisal puts current market value at $250,000. A lender advances 80 percent, or $200,000. At closing, $90,000 pays off the old loan. You receive $110,000. New loan is $200,000 at the new rate and term.

The numbers work because electrical gear, especially from manufacturers like Siemens, Powell, and Square D, depreciates slowly relative to most industrial equipment. A piece of switchgear that financed at $400,000 five years ago may still appraise at $300,000 or more with proper maintenance. That durability is what makes cash-out feasible long after the original purchase.

The new loan's interest rate may differ from the original depending on market conditions and the borrower's current credit profile. Rate is one consideration. The net capital received and its productive use should be weighed against the monthly payment increase on the larger new balance. Cash that goes to work on a profitable project justifies a rate above the original. Cash that sits in a checking account does not.

Why Operators Pull Cash Out

There is no one reason. Some of the situations we see most often:

- Funding the capital stack for a new project. An electrical contractor with equity in a piece of gear can use a cash-out refi to fund materials procurement on the next job, rather than drawing on a bank line or bringing in a partner.

- Bridging a payment gap. Progress billing leaves contractors cash-short between billing milestones. Equity in owned gear can bridge that gap without taking on unsecured debt at higher rates.

- Investing in additional equipment. The cash-out proceeds fund a down payment or deposit on new gear. An industrial operator can monetize existing switchgear to help acquire a new motor control center or additional distribution equipment.

- Funding a business expansion that a bank will not move quickly on. A contractor landing a large contract can access their equipment equity faster than a bank can process a new line of credit application.

The key question to ask before proceeding: is the monthly payment on the new, larger loan manageable given current revenue? Cash today at a higher monthly cost only makes sense if the return on the capital deployed justifies the additional debt service.

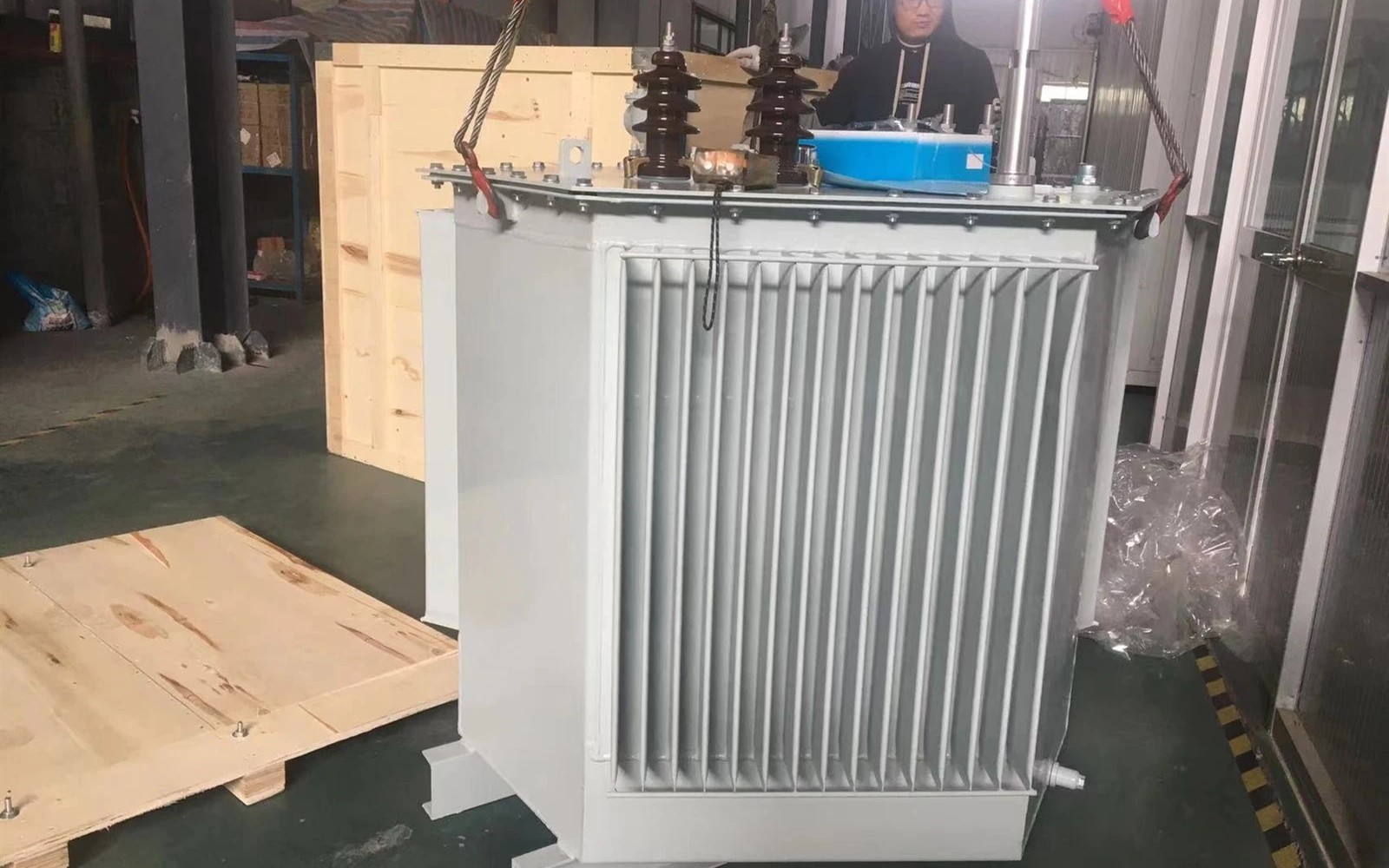

What The Appraisal Looks At

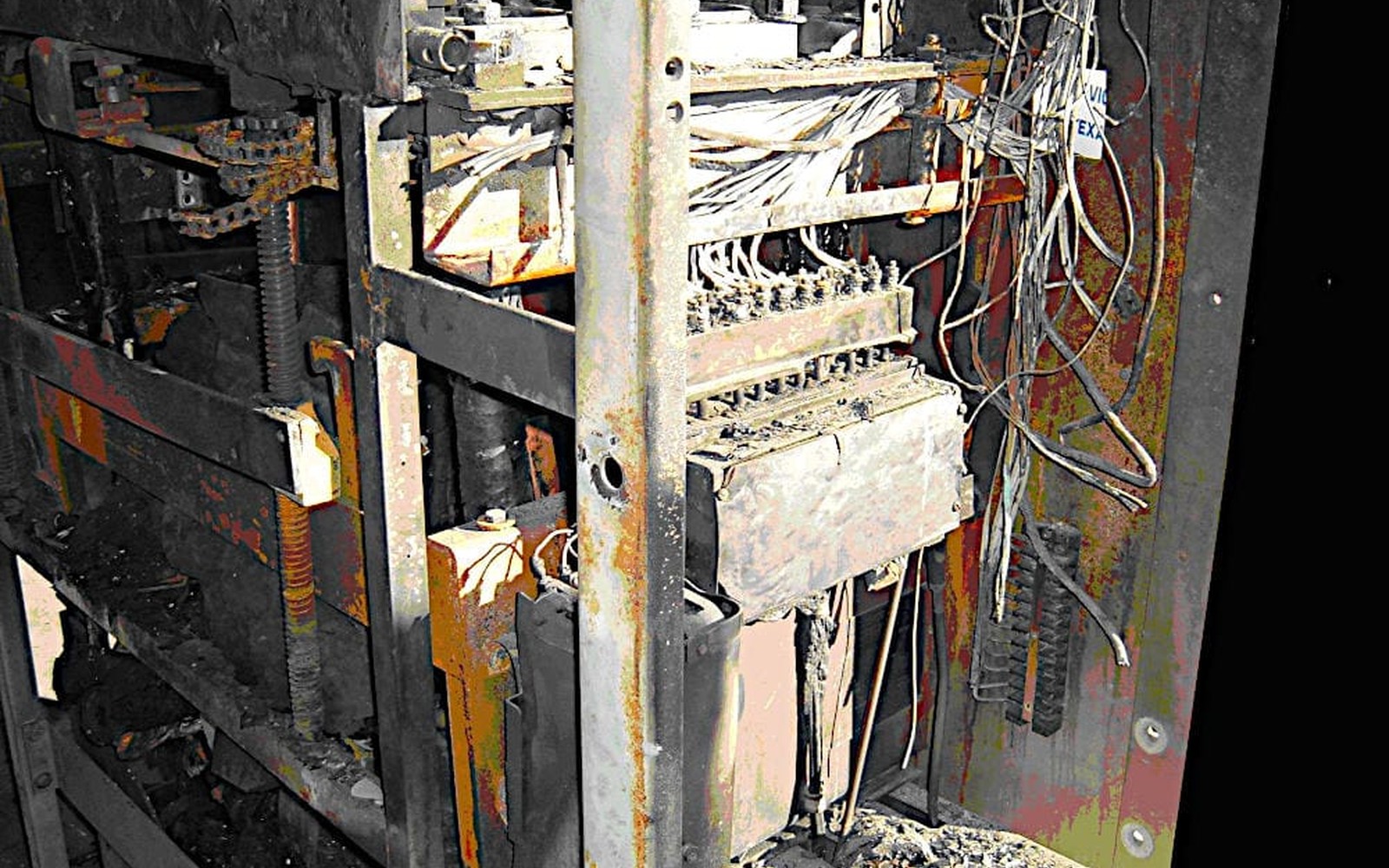

A switchgear appraisal for a cash-out transaction covers several factors: original manufacturer and model, voltage class and amperage rating, age, maintenance history, and condition of key components including the bus, circuit breakers, protective relays, and enclosure. Gear in active service with documented annual inspections appraises significantly better than gear that has been sitting idle or has deferred maintenance.

The appraiser will also look at secondary market demand. Certain asset types have strong reconditioning markets, including metal-clad switchgear and arc-resistant switchgear from major manufacturers. Niche or highly customized assemblies are harder to value because the secondary market is thinner. If your gear is highly customized for a specific process application, expect a more conservative advance rate.

Units in utility and cooperative applications often have long documented service histories that support strong appraisals. Oil, gas, and petrochemical operators running gear in classified locations have assets that require specific appraisers familiar with hazardous-location ratings, but those appraisals can be arranged. The critical input is providing accurate maintenance records and original specification documentation from the purchase. Missing documentation does not kill the deal but can reduce the advance rate.

What You Need To Apply

Required documentation for a cash-out refi:

- Equipment description: manufacturer, model, serial number, year of manufacture, current location

- Existing loan payoff statement

- Three months of business bank statements

- Maintenance records and most recent inspection report if available

- Business financials may be required depending on total loan size

For transactions under $400k where the existing loan is current, we can sometimes run an Application-Only Financing underwrite. Check the application-only financing page to see if your situation qualifies. For larger transactions, full underwriting is the standard path.

Gear that sits free and clear, with no existing lender to pay off, is the simplest cash-out scenario. The full advance amount minus origination costs goes to the borrower. No payoff coordination is required. For gear with an existing loan, we coordinate directly with the current lender to arrange payoff at closing, which simplifies the process for the borrower. You do not need to pre-pay the existing lender out of pocket; the refinance transaction handles it in sequence.

Timeline from application to funding on a cash-out refi typically runs two to three weeks, slightly longer than a standard equipment purchase because the appraisal step adds time. For equipment with a strong, well-documented pedigree, appraisals can come back within a few days of the inspection.

Cash-Out Vs. Sale-Leaseback

Both a cash-out refinance and a Sale-Leaseback Financing turn equipment equity into working capital. The mechanics differ in ways that matter for the balance sheet and for long-term ownership.

In a cash-out refi, ownership stays with the borrower. The loan appears as a liability and the equipment stays as an asset. Depreciation continues on the owner's books. At the end of the loan term, the equipment is fully owned. In a sale-leaseback, ownership transfers to the financing company. The equipment comes off the balance sheet. The company leases it back under an operating arrangement and makes lease payments rather than loan payments. At the end of the lease, ownership may or may not transfer back depending on the structure.

Neither option is universally better. Cash-out refinancing makes sense when you want to retain ownership and the monthly payment increase is manageable. Sale-leaseback makes sense when balance sheet management or immediate cash generation is the priority and long-term ownership is less critical. We can model both structures on the same piece of equipment if the decision is not obvious.

Price This Switchgear Financing Package

Send the quote, seller, lead time, deposit requirement, project location, and the electrical package scope. We will review the structure around the purchase schedule.

Review Switchgear TermsCommon Questions on Cash-Out Refinancing for Switchgear

Straight answers before you send the equipment file.

Is there a minimum equity percentage required before I can cash out?

Most lenders want the new loan to stay at or below 75 to 85 percent of appraised value. If your existing payoff is already at 90 percent of value, there is not much equity to extract and the transaction cost may not be worth it.

Does pulling cash out of equipment affect my ability to finance new gear?

It adds debt service to your financial picture, which underwriters will see. A cash-out refi does not automatically disqualify you for new equipment financing, but the new monthly obligation gets factored into your debt coverage ratio for future deals.

Can I cash out gear that has never been financed before?

Yes. Gear you own outright with no existing loan is actually the cleanest situation for a cash-out. There is no existing lender to pay off, so the full advance amount minus closing costs comes to you.

How is cash-out refinancing different from a sale-leaseback?

In a cash-out refi, you remain the owner and the loan is secured against the equipment. In a sale-leaseback, you sell ownership to the financing company and lease the equipment back. Sale-leaseback removes the asset from your balance sheet; cash-out refi keeps it there.

Will the new interest rate be higher than my original loan?

Possibly, depending on when the original loan was done and current market rates. Rate is one factor. The cash generated and its productive use should be weighed against the rate differential on the full new balance to determine if the transaction makes economic sense.

Can I cash out a transformer or MCC rather than a switchgear lineup?

Yes. Pad-mounted transformers, dry-type transformers, and motor control centers all qualify for cash-out refinancing if they have sufficient appraised value relative to the existing debt. The asset category and manufacturer affect the advance rate, but the structure is the same as for switchgear.

Review The Cash-Out Refinancing for Switchgear Package

Send the equipment quote, seller, lead time, deposit schedule, and project location. The finance desk will review the package against the actual procurement calendar.