Switchgear Equipment

Circuit Breaker Financing

Circuit breakers are the component most likely to be the last thing specified and the first thing needed on a project. A breaker that does not ship on time pushes energization by weeks. Financing the order the same day the spec is confirmed keeps the procurement timeline intact and keeps the critical-path item moving.

Low-voltage power circuit breakers, molded-case breakers, and medium-voltage circuit breakers all qualify for equipment financing. The range is wide: a single large low-voltage power circuit breaker like an Eaton Magnum or a GE EntelliGuard can cost $15,000 to $60,000 individually, while a medium-voltage breaker for a 15 kV switchgear lineup can run $30,000 to $100,000 per compartment. Projects involving complete lineups with multiple breakers, draw-out mechanisms, and control wiring reach $200,000 to $600,000 quickly. Our minimum is $50,000, and application-only processing covers deals up to $400,000.

We finance standalone breaker procurement, breaker replacements in existing gear, and complete switchgear assemblies that include the breakers as integrated components. New, surplus new, and refurbished breakers with documented testing history all qualify.

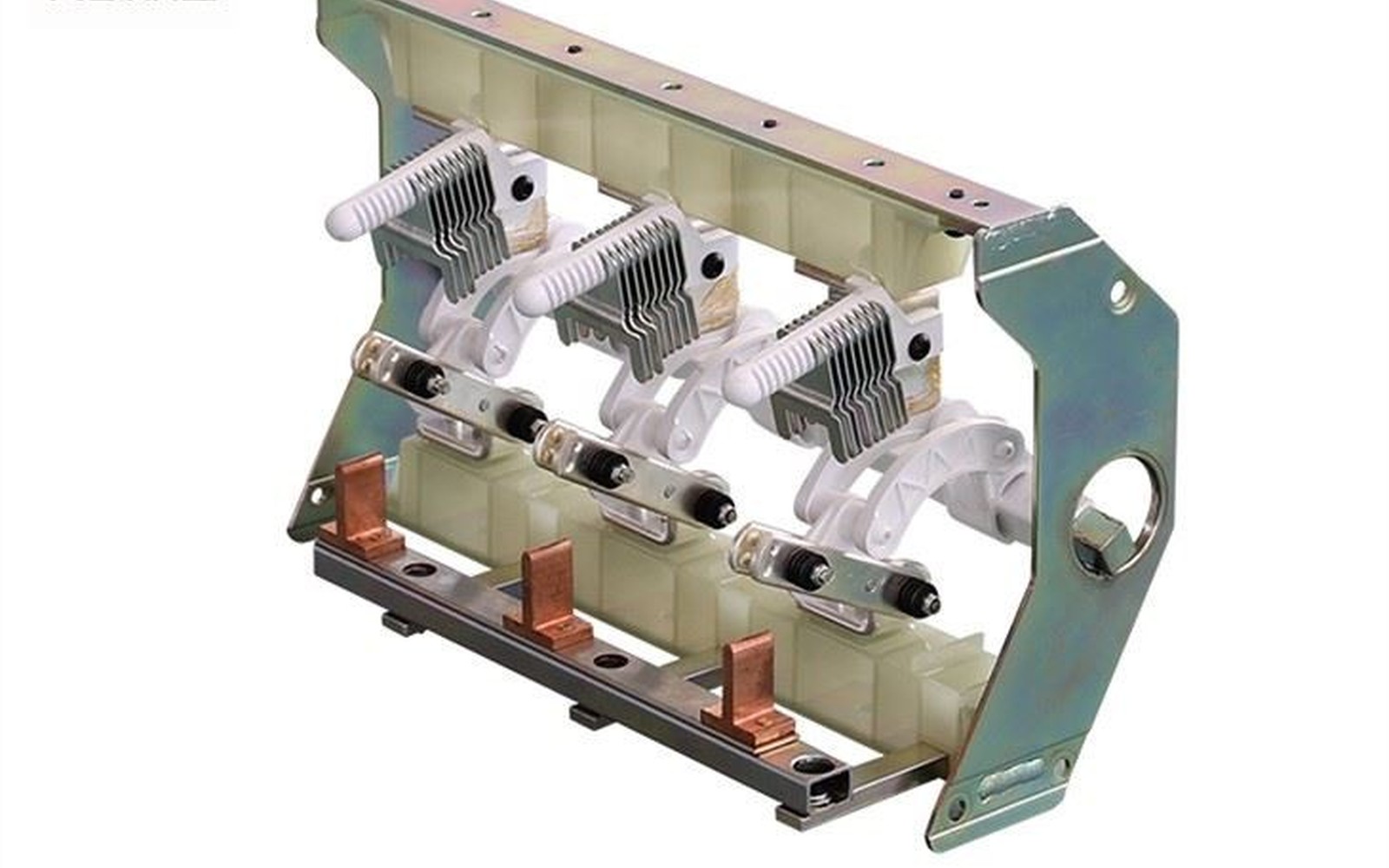

Low-Voltage Power Circuit Breakers Vs. Molded Case

Low-voltage power circuit breakers (LVPCBs) are the largest category by deal size. They are draw-out design, meaning they can be racked out of the switchgear lineup for maintenance or replacement without de-energizing the bus. Ratings typically run from 600A to 6000A at 600V or less. Because they are draw-out, individual breakers are replaceable in service, which gives them a strong secondary market and makes them a solid collateral asset.

Molded-case circuit breakers (MCCBs) are fixed-mount, lower-cost, and cover a broad range from 15A branch circuits up to 3000A main breakers. They appear in Switchboard Financing, Panelboard Financing, and motor control centers. Individual MCCBs are typically not financed as standalone items because their unit cost falls below our minimum, but large quantities of MCCBs in a switchboard or MCC lineup are routinely financed as part of the full assembly.

Insulated-case circuit breakers (ICCBs) sit between LVPCBs and molded-case in both cost and functionality. They appear in applications where draw-out is not required but electronic trip functions are. They share similar financing profiles with LVPCBs.

For projects requiring arc-resistant breaker assemblies in primary service applications, the gear qualifies under our arc-resistant switchgear program, which carries the same terms and timeline as standard circuit breaker financing.

New, Surplus New, And Refurbished Breakers

New breakers from the manufacturer ship with full warranty and current firmware on the electronic trip unit. They are the most straightforward from a financing perspective because condition and value are documented at the factory invoice.

Surplus new breakers are factory-new units that were purchased for a project that was cancelled, modified, or over-specified. They carry no hours and typically come with the original documentation and test certificates. Many buyers purchase surplus new breakers to reduce cost, and we finance them the same way we finance factory-new gear, provided the surplus source is an established distributor.

Refurbished breakers with documented test records, new contacts, and updated trip units are eligible under our used equipment financing program. The refurbishment documentation is the critical piece: a tested, re-certified breaker from a credible rebuilder has real value and qualifies. An unknown breaker without inspection records does not.

Credit And Documentation Requirements

For deals up to $400,000, the process is application-only. Fill out the application with basic business information, provide the vendor quote or purchase order, and we submit to underwriting. No tax returns, no financials required at this tier.

Larger deals typically require three months of business bank statements and, depending on deal size, additional financial documentation. B and C credit is reviewed on the full picture, including time in business, equipment value, and revenue consistency. A contractor with a strong backlog but a recent lean quarter is a different risk than a company with no booked work, and our underwriters understand that distinction.

Electrical contractors who finance breakers for specific projects can use the signed contract or purchase order as supporting documentation. This reinforces the credit profile significantly, because the asset has a known destination and a funded owner paying for it.

Why Breaker Procurement Is Tightening Lead Times

Circuit breaker lead times on large LVPCBs and medium-voltage breakers have extended over the past several years as demand from data center construction, grid modernization, and industrial reshoring has run ahead of manufacturing capacity. A large power circuit breaker that once shipped in four to six weeks may now require 20 to 40 weeks on a new-order basis from the original manufacturer.

This makes early procurement and financing more important, not less. Contractors and owners who lock in orders early with financing in place avoid the schedule risk entirely. Those who wait for budget approval to move through multiple layers of sign-off end up in the queue late and sometimes face energization delays that cost more than the financing interest would have.

For buyers in the data center and renewable energy sectors, where project commissioning dates drive revenue, this lead time reality makes equipment financing a risk management tool as much as a capital management tool.

Price This Switchgear Financing Package

Send the quote, seller, lead time, deposit requirement, project location, and the electrical package scope. We will review the structure around the purchase schedule.

Review Switchgear TermsCommon Questions on Circuit Breaker Financing

Straight answers before you send the equipment file.

Can I finance a single large draw-out circuit breaker as a standalone item?

Yes, provided the purchase price meets or exceeds our $50,000 minimum. A single large LVPCB or a medium-voltage breaker frequently meets that threshold on its own.

I need to replace a failed circuit breaker immediately. Can financing close fast enough to help?

Emergency replacements are a real scenario. We can move through the application quickly, and a straightforward deal can fund in under two weeks. For a truly same-day emergency, a corporate credit card or existing line of credit may be faster for the initial purchase, with a refinance to follow.

My application includes ten replacement breakers across three different voltage classes. Can those be on one financing request?

Yes. Multiple breakers across different voltage classes, packaged together as a single procurement, are financed as one deal. The total value is what drives the underwriting, not the number of individual units.

The breaker I need is no longer in production. I found a refurbished unit from a specialized rebuilder. Does that qualify?

Refurbished breakers from credible rebuilders qualify under our used equipment financing program. The key documentation is the inspection and test report, confirmation that contacts and trip units are serviceable, and the rebuilder's credentials.

Can I include shipping and rigging in the financed amount?

Soft costs, including delivery, rigging, and in some cases installation, can often be rolled into the financed amount up to a percentage of the total. This varies by program and deal size.

Review The Circuit Breaker Financing Package

Send the equipment quote, seller, lead time, deposit schedule, and project location. The finance desk will review the package against the actual procurement calendar.